Mainland appetite fuels ninefold growth in Hong Kong’s insurance sector in 20 years

Acquisitive mainland firms see Hong Kong-based insurance companies as a short cut to entering the city’s financial services sector

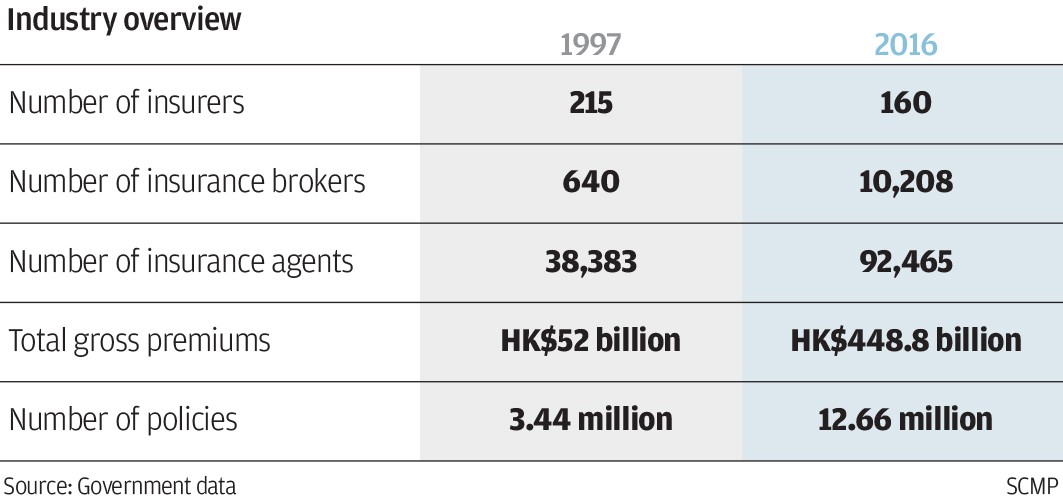

The insurance sector in Hong Kong has expanded ninefold over the past two decades, when measured by value of premiums, thanks to a mainland buying spree targeting life insurance products and the companies selling them.

The gross value of insurance policy premiums in 2016 stood at HK$448.8 billion (US$57.55 billion), up 763 per cent from HK$52 billion in 1997, according to government statistics.

By taking over Hong Kong insurance companies, mainland companies find it easier to obtain the licences they need to conduct a wider range of financial services

The number of policies had more than tripled in the same period, to 12.66 million last year from 3.4 million 20 years ago. And the number of sales agents in Hong Kong had also grown, by 141 per cent to 92,465 last year from 38,383 in 1997, when the territory was handed back to China by the British government.

“The growth of the insurance industry in the past 20 years has been because of economic development and the fact people are more concerned about insurance protection for themselves and for their families. It is also due to mainlanders who like to buy insurance products here because there is a greater choice of products and they tend to offer more attractive returns,” said Peter Tam, chief executive of the Hong Kong Federation of Insurers.

Mainlanders spent HK$48.9 billion buying policies in Hong Kong during the first nine months of last year, the latest available data from the government, representing 37 per cent of all life policies sold. That’s 26 times higher than the HK$1.8 billion they purchased in the nine months from April to December 2005, when the data was first published.